As they get to their 50s or 60s, nearing retirement or already retired, many buyers begin chasing earnings and ignoring development of their portfolio. This may appear logical, however it might probably spell hassle, and jeopardize their retirement.

You possibly can hearken to Mike’s Podcast

If you happen to’re considered one of these buyers, maybe all you care about is your dividend earnings, and also you’re not involved about complete returns (dividend + inventory value appreciation).

I perceive the necessity to know that you just’ll have sufficient earnings, within the type of dividends, coming in recurrently to maintain your way of life. I additionally grasp how easy it will be to have your earnings wants fulfilled completely by dividends; in spite of everything, if you happen to want $50,000 per 12 months and you’ve got $1,000,000 invested, construct your portfolio to generate a 5% yield in dividends, and also you’re completed! Nothing else to consider, simple, easy.

This considering comes from your portfolio as if it have been an annuity that you just constructed. An annuity is a contract that totally ensures that no matter capital you set in it, you’ll obtain a 5%, 6%, or 7% yield just about ceaselessly. However…

Dividends aren’t assured!

A dividend inventory portfolio just isn’t a assured annuity. Corporations can lower their dividend at any time as they’re beneath no obligation to maintain paying dividends. A enterprise paying a dividend is utilizing its additional money to reward you in your persistence and your belief in that enterprise.

Consider it like paying your youngsters an allowance to encourage them to handle their cash and recognize the worth of issues. What occurs if you happen to lose your job, and end up struggling to place meals on the desk? Do you proceed to pay their allowance however make them skip breakfast? After all not. You chop their allowance and use that cash for important spending whilst you discover one other job and proper the ship. It’s not nice and it’ll upset your youngsters, however it’s higher than not doing it.

Equally, if an organization is crumbling beneath a heavy debt burden, its income and revenue are falling, and/or its free money move just isn’t sufficient to pay the dividend, reducing the dividend is the accountable factor to do. For retirees although, a dividend lower is at finest upsetting, disturbing, and at worst a hazard to their high quality of life. Additionally keep in mind that dividend cuts are sometimes accompanied by a drop within the inventory value, so buyers lose on each dividend earnings and inventory worth. Ouch! See Sniff Out Dividend Cuts.

Get nice inventory concepts in our Rock Stars checklist!

The dangers of excessive yields

When all the businesses that pay excessive dividend yields, we see that it’s simple to construct a high-yield portfolio. Nevertheless, I’d argue that at round 5% yield, it’s getting too excessive. Why? There’s no free lunch in finance; firms to pay excessive yields for a purpose, and it’s not out of the kindness of their hearts. That’s not the way it works in the marketplace.

Corporations pay a excessive yield as a result of the market doesn’t consider within the development of these companies. Why does that matter to you if you happen to’re unconcerned with development?

I’m a enterprise proprietor. Let me let you know that if my enterprise doesn’t develop continuously and reaches a plateau, it’s stagnating. Plateaus don’t final lengthy; you both provide you with new development vectors to thrive once more, otherwise you decline. Would you like a portfolio stuffed with declining firms?

What normally occurs with firms that pay a excessive yield however fail to search out methods to develop? Finally, they undergo after which undergo some extra. It will get to the purpose the place they haven’t any alternative however to put off employees, restructure the group, and ultimately lower the dividend. Dividend cash isn’t free, and they should reallocate that cash to guarantee that the enterprise can get well and thrive once more, or maybe simply to save lots of the enterprise for a number of extra quarters.

Keep in mind AT&T?

AT&T was a dividend aristocrat displaying greater than 35 consecutive years of dividend improve. You understand what occurred with AT&T: the inventory value fell, and it lower its dividend. By no means take dividend earnings without any consideration. Chasing earnings and ignoring development is a really dangerous play as a result of while you undergo the dividend lower, you in all probability additionally lose inventory worth.

Get nice inventory concepts in our Rock Stars checklist!

What’s an investor in want of earnings to do?

So, what do you do? Swap your total portfolio round to solely deal with 1% and a pair of% yielders? Not essentially. You possibly can construct a portfolio with 3% and 4% yielders. That might be a very good steadiness.

If earnings is your essential concern, your consideration shouldn’t be on the dividend yield, however moderately on a set of metrics that present the well being of the dividend. This is smart for all buyers no matter age. You would possibly sacrifice 1% or 2% in yield, however you make sure that:

- The dividend will proceed to be paid

- Extra importantly, the dividend will proceed to extend and match inflation. $10,000 at the moment and $10,000 in 15 years received’t final you as lengthy, proper? You don’t need to lose your shopping for energy down the street.

I consider the most secure method to construct a portfolio, even in retirement, is to focus on dividend growers and have a sizeable portion of your portfolio in low-yield, high-growth shares which are thriving. That’s my technique, and I’ll keep on with it for the following 40 years or extra. Another excuse is that I don’t solely make investments for myself however for my partner, my youngsters, and someday my grandchildren. In consequence, I’ll preserve a long-term investing horizon, even in my 70s or 80s.

Takeaway

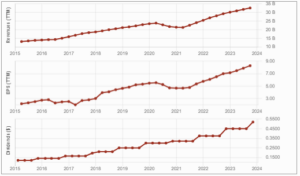

We see that chasing earnings and ignoring development can result in massive issues. The important thing level to spare your self the ache is to keep away from stagnating and declining firms by verifying that the dividend is wholesome. Evaluate the dividend triangle, the payout ratio, and the development of dividend development to see if it’s accelerating, slowing down, or worse, stagnating. For extra particulars, see Detect Losers and Find Winners with the Dividend Triangle.

Purple flags? An organization whose administration “forgets” to develop its dividend for a 12 months, dividend development that’s slowing down, and a excessive yield. With these, you’re one step away from a dividend lower and from shedding worth om prime of earnings. There’s no getting back from this. As all the time, additionally observe the development of income and EPS to make sure development vectors exist and work.