Rate of interest cuts are coming. We’ve been listening to that for the reason that fall of 2023. Hasn’t occurred. How come? Extra worrying for buyers is what’s going to occur, and how you can put together.

Within the fall 2023, with inflation easing and the financial system on the whole seemingly beneath management, it made sense for the Federal Reserve and economists to anticipate rate of interest cuts for the brand new yr. With all this optimism, many buyers who had shied away from the inventory market, preferring bonds or certificates of deposits—which provided their most first rate returns in years—or who have been on the sidelines, went on a buying spree. They flocked to the market, purchased a whole lot of inventory, a inventory costs went up.

Learn to create a recession-proof portfolio. Obtain our free workbook.

Why no rate of interest cuts but?

What occurred subsequent is that inflation went again up a bit moderately than persevering with to abate. The month-to-month inflation price within the U.S. went from 3.1 in January 2024, to three.2 in February, then to three.5% in March. Whereas significantly better than the above 6% figures we have been seeing a yr in the past, and higher than the common of 4.1% for 2023, the Fed thought, “Hm, we want a bit extra time earlier than we lower rates of interest.” And right here we’re.

What’s taking place now?

Unemployment charges have began to extend in fall 2023 however solely barely. There aren’t any alarming indicators of shoppers feeling squeezed sufficient to cease discretionary spending altogether. The U.S. financial system is extra resilient than anticipated. That could be a good factor as a result of it reduces the percentages of a deep recession.

Nonetheless, there are indicators of a slowdown. We see them in quarterly company earnings. Company earnings can be found extra rapidly than financial information revealed by the Fed and authorities departments, which at all times lag behind as a result of time required to collect and compile the information. The impression of a slowdown is extra instant for firms. They see their gross sales development slowing down or gross sales falling. Their margins undergo, as do their earnings and the free money stream they’ve available.

What I anticipate will occur

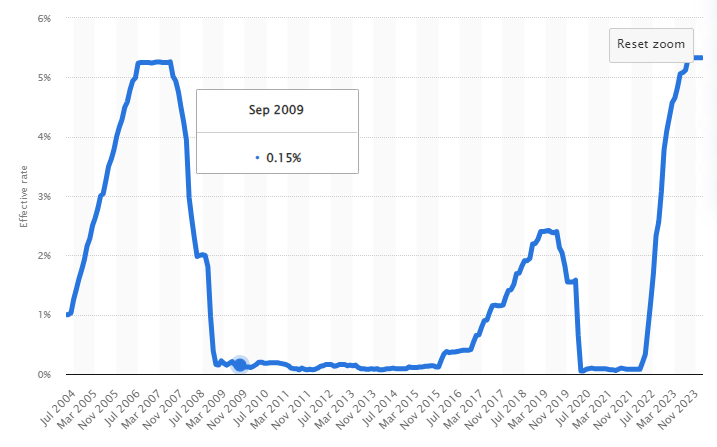

In these situations—inflation easing step by step and indicators of a slowdown—I’ve little doubt rate of interest cuts are coming later in 2024. Nonetheless, I can’t see us going again to the historic lows we loved from 2009 to 2017 or to the under 2.5% charges of 2018 to 2022. The cuts will probably be small, come slowly and steadily.

Reasonable rate of interest cuts will present some reduction to owners having to resume their mortgages. A lot of them nonetheless benefit from the tremendous low charges of pre-2022 and can renew from 2024-2026. They are going to accomplish that at charges that will probably be decrease than they’re now, however larger than what that they had. So, whereas their funds may not double, they’ll nonetheless go up. Just a few hundred {dollars} extra per thirty days on a mortgage cost means just a few hundred fewer {dollars} spent on eating places, new vehicles, and journey.

We’re already seeing firms within the shopper discretionary sector with weaker outcomes and that can proceed. Firms in different sectors are additionally feeling the slowdown.

Getting ready for what’s coming subsequent

As an investor, I don’t commerce for concern of short-term financial occasions, slowdowns, and even recessions. What I do is dutifully evaluation my holdings, as we should always all do quarterly. I evaluation my sector allocation and particular person inventory weight and regulate if wanted. I evaluation every holding to make sure that that they had wholesome development tendencies over the past 5 years, that the dividend is protected, and that my funding thesis for holding them remains to be legitimate. See Quarterly Review of Your Stocks Made Easy.

I’ll additionally establish which shares would be the most affected by a downturn. Realizing that, when my portfolio goes down, I perceive it and I don’t fret. For instance, I do know my shopper discretionary holdings will damage, in the event that they don’t already. I don’t anticipate them to carry out very properly for the following 12 to 18 months. However I’ll evaluation them to make sure they’re in a robust place to climate the storm and are available out of it swinging.

Be prepared, create a recession-proof portfolio. Obtain our free workbook.

Abstract

We’re seeing the market slowing down with returns under expectations, largely as a result of the market anticipated rate of interest cuts sooner. We would have to attend till Might or June to see cuts.

On the upside, we have now a resilient financial system; sure, meaning we’ll seemingly see solely reasonable rate of interest cuts, but additionally, we most likely gained’t have a deep recession. Avoiding an enormous recession means the inventory market shouldn’t crash. That is what I anticipate, and what I hope, however we by no means know what the long run holds.

One of the simplest ways to guard your portfolio towards no matter occurs is to make sure that you’ve gotten very sturdy companies with stable metrics. Overview all of your shares, wanting on the dividend triangle; guarantee they present tendencies of rising gross sales, earnings, and dividends, and have the enterprise mannequin and development vectors to proceed doing so. You may additionally wish to evaluation the composition of your portfolio.

If the worst occurs, figuring out the strengths of your holdings will forestall you from panic-selling at a loss for no cause, and make you a affected person investor.